Portfolio Musings

I did some rebalancing recently and thought I'd pin how I'm positioned going into the new year.

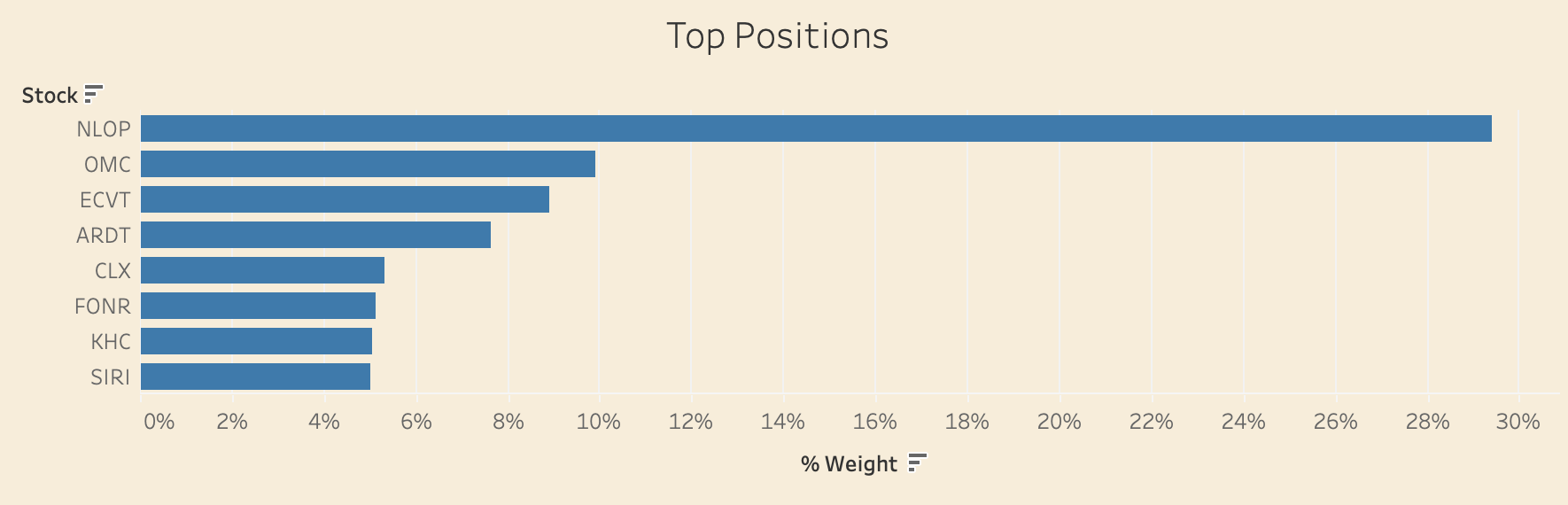

The below chart makes up three quarters of my portfolio, with the remainder comprised of another 17 longs and some hedges/puts.

Net Lease Office Properties (NLOP) - 29.4%

NLOP has been written up in several places but the one-liner is it's a liquidation play. I expected a 12-17% after-tax IRR in 2-3 years when I bought the position, and despite aggressive stress testing, found it hard to see losing more than 10% of my money in a worst case scenario. Since I've owned it, they distributed $3.10 in September and just announced another $4.10 to be distributed in December.

source of idea: Lone Elm Capital (he provides his paid subs access to his spreadsheet of properties / estimates etc) and Kingdom Capital Advisors

Omnicom Group (OMC) - 9.9%

I published my thoughts on OMC here. Pro forma, it trades at a single-digit multiple of normalized free cash flow for a predictable business that, 1) generates a lot of cash with minimal capex and negative working capital, 2) could see efficiencies with AI, and 3) is targeting $750M cost savings post-merger.

Ecovyst (ECVT) - 9.0%

Ecovyst is another I wrote about here. They're the North American market leader in chemical recycling for refineries, with a business model that supports 70%+ cash conversion, stable/durable margins, a pro forma clean balance sheet, and a capital return profile that could retire 10% of the shares outstanding per year while I wait for longer-term tailwinds + margin expansion or a takeout.

Ardent Health (ARDT) - 7.6%

Ardent Health is a company I've been watching since July when my friend Karst Research mentioned it. Ardent provides healthcare services through their network of hospitals, urgent cares and other various clinics and centers.

In November, they reported earnings that disappointed due mostly to unexpected increases in costs, with the stock declining ~40%. My view is that runaway costs are temporary, not permanent – whether that's 2 quarters or 2 years is less certain. But, the underlying business is performing well and valuation is undemanding.

I think they'll do a little under $190M FCF, against a market cap of $1.3B.

They have $1.1B debt and $600M cash – if I want to be extra conservative and include self-insured liabilities and leases as debt, I end up with ARDT trading at fair value. So, if runaway costs persist, I think the valuation can absorb quite a bit.

The big risk is the execution of potential acquisitions. If it were up to me, I'd split FCF between buybacks and deleveraging. In 5 years, you're net debt free, retired 20-30% of the shares outstanding and probably trade at a premium. At which point you could use your stock as currency to acquire something. I digress. Management did authorize a $50M repurchase program last week, though.

All else equal (always a fun phrase), I think ARDT is worth twice where it currently trades – so about $18 per share.

Clorox (CLX) - 5.3%

Clorox needs little introduction. A boring consumer products company that is normalizing after everyone wanted disinfectant wipes during covid. They own Clorox, Glad trash bags, Hidden Valley Ranch, Kingsford Charcoal, cat litter and more. It trades at a fair price, has good returns on equity and tangible assets, pays a 5% dividend and has a strong balance sheet. In my view, they're an attractive acquisition target, but I'm happy to hold.

FONAR Corp (FONR) - 5.1%

I wrote about FONAR here. In July, the company received a non-binding proposal from its CEO, Timothy R. Damadian, to acquire the outstanding shares of the company in a going-private transaction for $17.25 per share in cash – a 20% premium to the current stock price. It's not a very liquid security, but I've been adding shares since the price has declined since August, taking my position from 2% to 5%. While we haven't heard anything yet on the deal, I still think it's a good bet and expect an announcement sooner rather than later.

Kraft Heinz (KHC) - 5.1%

Similar to Clorox, KHC needs no introduction. Berkshire Hathaway is a bag holder and the stock seems to be on a singular trajectory to find earth. Fortunately, CPG companies rarely exist in their then-present form for long. When in doubt, CPG's resort to mergers, acquisitions and/or divestitures. Indeed, Kraft and Heinz are (more or less) getting a divorce, which is fine by me (though, Buffett sounded unopposed to the idea of getting bought out of his position completely).

Kraft has been dragging down performance of the overall company for years. Nonetheless, I think it trades at a fair price, has good returns on tangible assets and pays a decent dividend. There are consumer headwinds, but there are cycles to everything. I've joked I'm happy to buy a perpetual royalty on ketchup – we'll see how long I hold it.

SiriusXM (SIRI) - 5.0%

Everyone knows what SiriusXM is – it's the thing that is built into every new car, only boomers use, and Spotify subscribers hate. I'm a sucker for companies that everyone hates and generates a lot of cash. Despite SIRI being a zero that will never hit any of their cash flow targets, they've increased FCF guidance several times this year.

The company has a market cap of $7.5B, is going to do $1.225B FCF and is on a path to do $1.5B in 2027. The best part (in terms of predictability) is it doesn't rely on growth, it relies on a reduction in their capex cycle. When I first bought SIRI, I used $950M as my normalized FCF target. So, I'm "happy" as long as they generate $950M.

They're going to generate $1.225B, and most likely will hit $1.5B. But if they don't – if they reduce the capex but spend all the "savings" on increased content spend or paid subscribers declines dramatically – there's a lot of room to absorb that before I get concerned.

I expect little else for the next several years aside from them focusing on deleveraging (they have $10B of debt, with maturities every year for the next several years). Berkshire Hathaway owns a large chunk. I'm not expecting them to acquire it per se, though it is the type of asset that is best being acquired, harvesting the cash flows and investing somewhere else. Cheap, hated, leveraged cash flow – my favorite.

Remainder / Summary

The rest of my portfolio includes one of my favorite companies I hope to hold forever, plus some more take-privates, tracking positions and small puts and hedges (can't help but scratch that itch).

Overall, my theme is cheap, predictable/durable and (relatively) uncorrelated cash flows. NLOP is my most predictable position. It's basically a bond that will mature in a couple years and earn a good yield, and answers my three favorite questions:

- How much cash is there?

- When will I get it?

- How sure am I?

That's in the face of what I consider a market filled with participants who have little concern for, or ability to recognize and price, risk. We've all seen it, and thanks to human nature, have become accustomed to it.

Someone recently said of NLOP that a setup with no downside (except for the possibility of underperforming the market) and 10-14% IRR upside was "meh."

If you think a situation with almost no chance of permanent loss of capital and 10-14% upside IRR is "meh," it's hard for me to take you seriously (which is okay, I'm not that serious of a person anyway). There seem to be a lot of people who don't understand the game they're playing. Sign of the times. Or, maybe that's how it always is.

I've also been (half) joking with friends recently that there is a problem brewing in credit.

For example,

The broadly syndicated loan market has enjoyed a fairly steady climb as well, reaching a high of $1.4 trillion in September 2022 before leveling off and dipping slightly in 2023.

About 80 percent of broadly syndicated loans...are covenant-lite – i.e., they do not feature financial covenants requiring a borrower to show a minimum annual cash flow in comparison to the amount borrowed, as has typically been the case in the past. That is reflective of a market that has become more amenable to the borrower in recent years. – Saratoga (emphasis mine)

There's a lot of signs of lax market conditions. Nonetheless, what you look for, you will find. Markets go up over time. Trying to predict bubbles or short expensive stocks, in aggregate, costs more than it saves (at least for me). So, I'm trying to thread the needle of decent returns while maintaining cash flow and liquidity to take advantage of whatever comes.

Member discussion