Forward Pharma A/S (FWP)

Introduction

This was a situation I got into in 2017 that resulted in ~50% absolute return in a few months, and is one of the few times I feel comfortable saying the market was inefficient and there was a near-zero chance of losing money.

Here was the bet.

Background

In October 2004, Forward Pharma filed a Danish patent.

A decade later, Forward Pharma launched a $221M IPO in October 2014 “with eyes on unseating Biogen.”

In April 2015, the U.S. Patent Trial and Appeal Board (PTAB) declared a patent interference between FWP and Biogen. The dispute was over whether Forward Pharma or Biogen was the first to claim a certain treatment for multiple sclerosis (MS) – referring back to the FWP Danish patent from 2004.

In November 2016, oral arguments for the Patent Interference case were held, and by January 2017, Forward Pharma and Biogen signed a major settlement and licensing agreement, which had two important points:

- Forward Pharma agreed to license its intellectual property to Biogen. In exchange, Biogen would pay Forward Pharma a one-time, non-refundable cash payment of $1.25B.

- Forward Pharma agreed to only receive future royalties on U.S. sales if it won the ongoing Patent Interference case.

The License Agreement required approval from shareholders, with the payment to be made within five days of the extraordinary general meeting assuming approval.

Forward Pharma management said,

This agreement limits our downside risk should we not be successful in either the US or European proceedings and it provides clarity as to our royalty stream should we be successful in either or both of those proceedings.

Critically, the press release stated that

Forward is evaluating the most efficient way to deliver directly to its shareholders a substantial portion of the cash it will be receiving from Biogen. The Board is considering both stock buybacks as well as cash distributions.

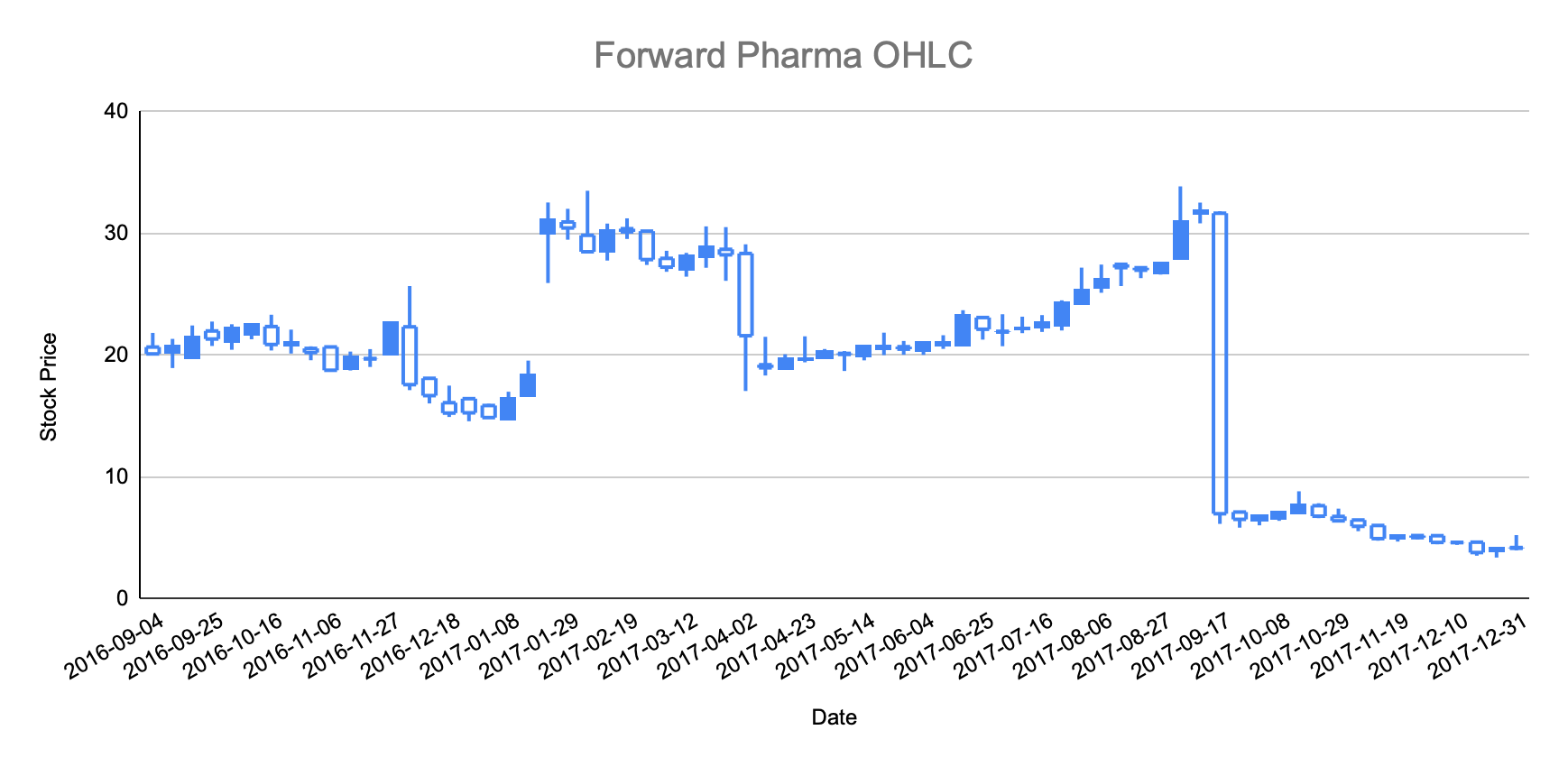

The announcement caused FWP stock to close the month of January up over 100%.

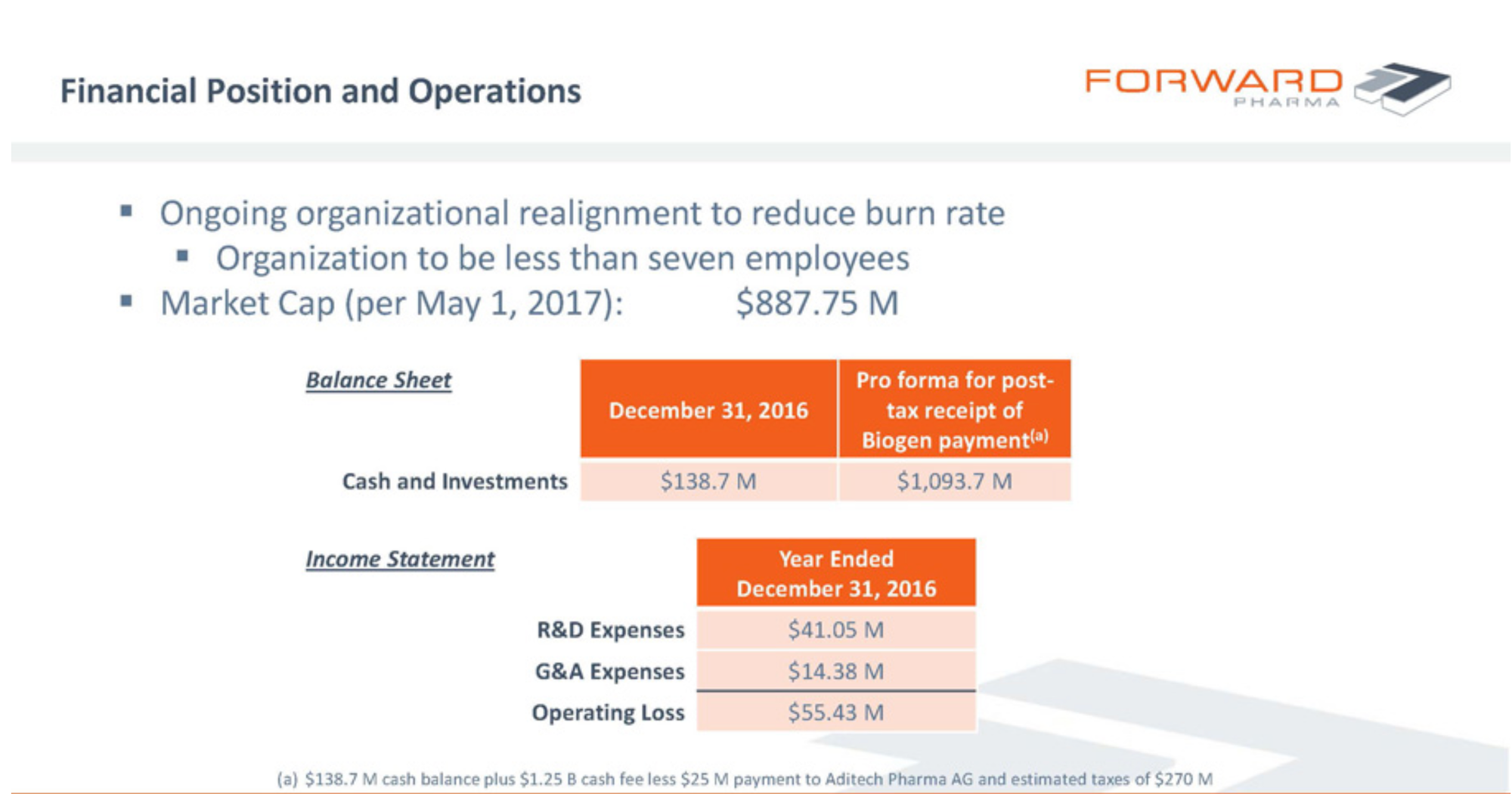

On February 1, 2017 the license agreement went into effect and FWP received the $1.25B cash payment, less a 22% Danish corporate tax and 2% owed to an affiliate.

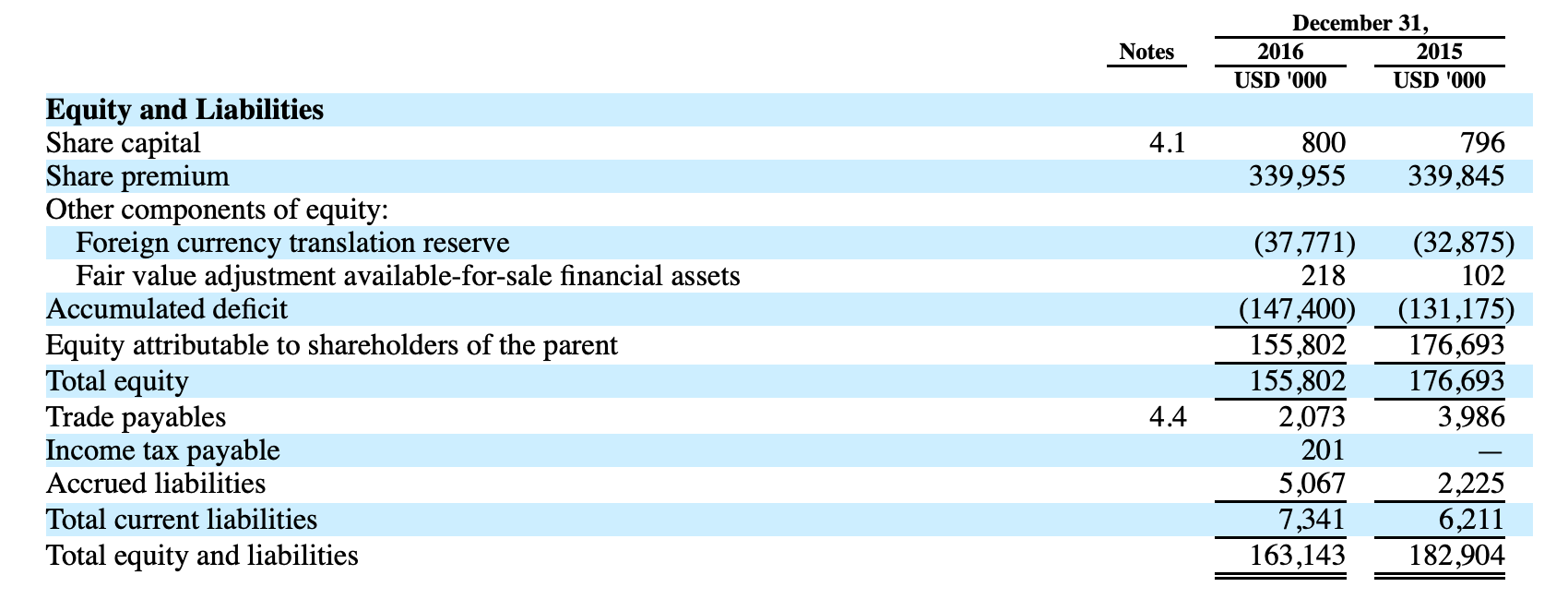

As context, at year-end 2016, FWP’s balance sheet primarily consisted of $58M cash, $81M available-for-sale financial assets (mainly German and U.S. government debt) and a deferred tax asset.

Total equity was ~$156M. Total liabilities were ~$7M.

Of course, biotech companies can look cheap until you look at the cash burn. That was around ~$35M for both 2015 and 2016.

Opportunity

At the end of March, PTAB issued a judgement in favor of Biogen, closing Forward Pharma’s possibility of future U.S. royalties.

The stock effectively got cut in half. And that created the opportunity.

FWP filed their 20-F April 18th, and a corporate update presentation on May 4th. With up-to-date information, the stock was selling for around $19 per share and they had over $23 per share of pro forma cash and investments against just 15 cents per share of total liabilities. Previous annual cash burn was around 70 cents which management was planning to reduce.

A definitive plan on how FWP was going to return the cash to shareholders was slated for the second quarter of 2017.

I took a position in May at a cost of under $20 per share. A few months later, shareholders approved a planned capital reduction and received a ruling from Danish tax authorities so that the company would not be withholding any part of the proceeds from the capital reduction for Danish tax.

I received a $23 per share return of capital distribution in September and sold the stub for $6 for an absolute return of ~50% and XIRR of ~275%.

Why'd the opportunity exist?

The patent case loss pushed down the stock below the net cash that was going to be distributed.

This wasn’t a micro cap stock. The company had a billion dollar market cap. However, the chairman, a director and a hedge fund – Baupost Group – collectively owned around 90% of the company. So the float was significantly less.

Interestingly, at the time, nobody was talking about this situation. I was early in my investment career and wanted to compare notes in case I was missing why this wasn’t an obvious mispricing, but I couldn’t find anyone. I wrote it up on a popular investing blog site but received zero interactions.

Maybe it was because it was a Danish company. Or a biopharmaceutical. In any case, it worked.

The Framework

As I never shut up about, the three questions to answer in investing are 1) how much cash is there, 2) when will you get it, and 3) how sure are you?

It took very little IQ to answer for FWP. The cash was already there. Management told me they were going to give most of it to me.

Even if there was withholding tax and I haircut the distribution, it was hard to see how I would lose money. And I didn’t see any reason why it’d take more than a year for the return of capital to take place.

Summary

Despite being a biopharmaceutical company involved in legal proceedings, it was a pretty straightforward situation.

A company received a nonrefundable fee that management said they’d return directly to shareholders.

Adverse legal proceedings around patent issues pushed the low-float stock below net distributable cash.

And the opportunity paid out exactly as expected.

These are my favorite types of bets. A simple situation with a catalyst to return cash in a short amount of time that no one cared about.

Member discussion