Ecovyst (ECVT)

Ecovyst (ECVT) is the North American market leader in chemical recycling for refineries, with a business model that supports 70%+ cash conversion, stable/durable margins, a pro forma clean balance sheet, and a capital return profile that could retire 10% of the shares outstanding per year while I wait for longer-term tailwinds + margin expansion or a takeout.

What They Do

Ecovyst has two segments:

- Ecoservices

- Advanced Materials & Catalysts

The latter is being sold – we’ll get to that later – so I’m only going to talk about Ecoservices.

Ecovyst is North America’s largest recycler of spent sulfuric acid. Sulfuric acid is one of the most important industrial chemicals in the world (so they tell me – and by ‘they,’ I mean Google). It’s used in refining, mining, wastewater processing, fertilizer manufacturing, paper, paint, batteries, etc.

Fun fact: Venus has a cloud layer of sulfuric acid that covers the entire planet, which is one of the reasons why it’s so hard to study (that, plus the surface is 460°C (860°F) and the surface pressure is 93x greater than Earth’s – equivalent to being 900 meters (3,000 feet) underwater).

Anyways.

Refineries use sulfuric acid as a catalyst to produce high-octane gasoline. The acid doesn’t get used up but becomes “dirty” or “spent” with contaminants. That spent acid has to be bled off continuously or the unit stops working. Once a refinery has chosen sulfuric acid alkylation, sulfuric acid regeneration isn’t optional. The spent acid has to go somewhere.

The refinery has a few options:

- Dump it somewhere – just kidding, you can’t do that (anymore) [legally]

- Build and run its own sulfuric acid regeneration unit on-site (expensive, capital/operation/regulatory intensive)

- Use a service like Ecovyst to “regenerate” it and send it back to use again (ie recycle it)

It's kind of like Bill Gates' funded device of converting poop to water — only completely different (don’t drink acid…or poop water, unless you have to…but never acid).

As far as I can tell, the only way around sulfuric acid regeneration is to repurpose the refinery from sulfuric acid alkylation to something else. Traditionally, the alternative to sulfuric acid was hydrofluoric acid, but there’s also R&D around ionic liquid and solid-acid alkylation methods. Regardless, you’re looking at a major capex project and change in strategy on how a refinery wants to make octane.

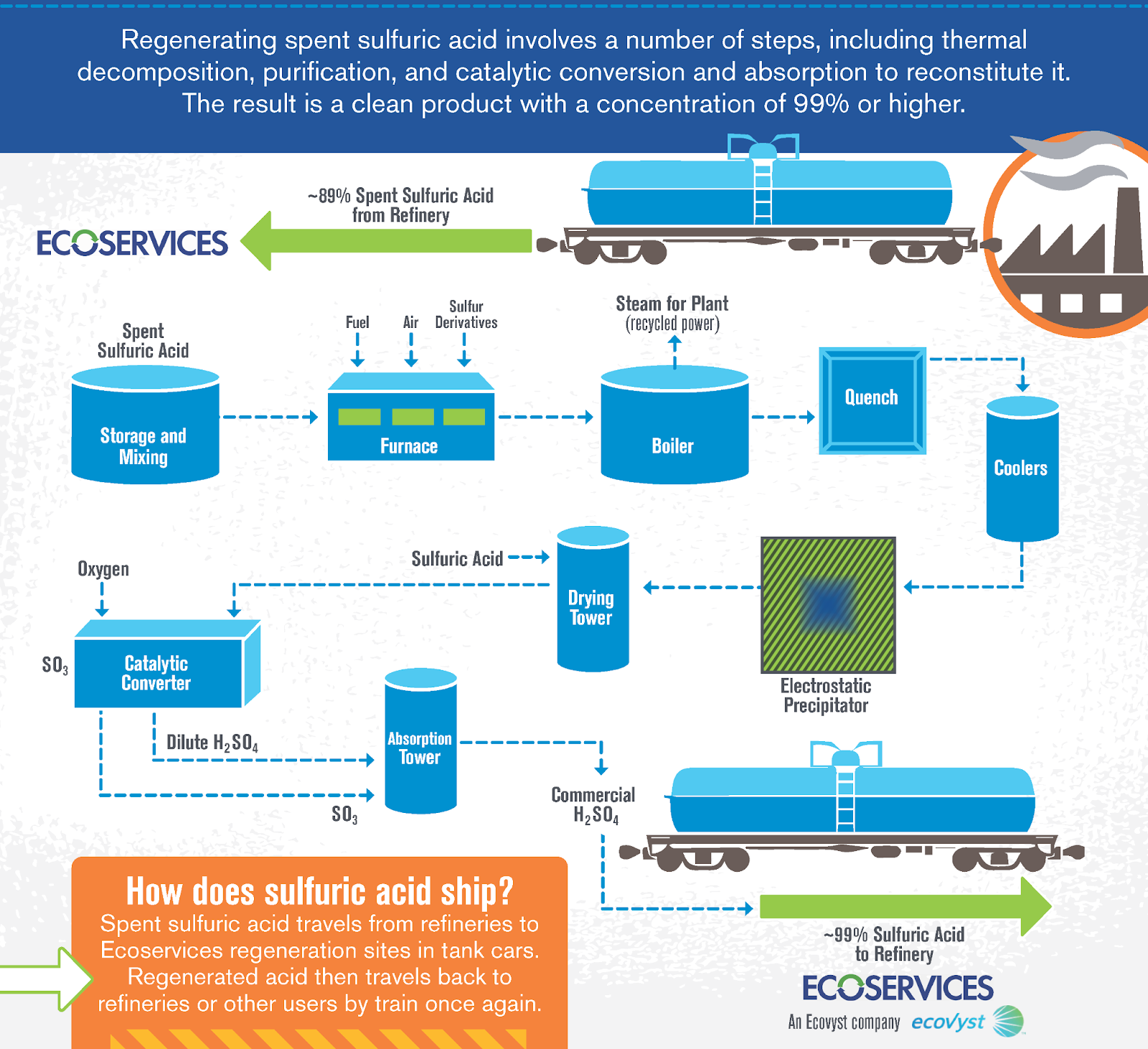

So, the circle of life for us is, 1) a refinery uses sulfuric acid, which 2) bleeds off spent acid, which 3) Ecovyst takes and turns into 99% regenerated acid and 4) gives back to the refinery to use again.

It’s a bit more technical than that – but that’s about all my brainwidth can handle. Here’s a visual:

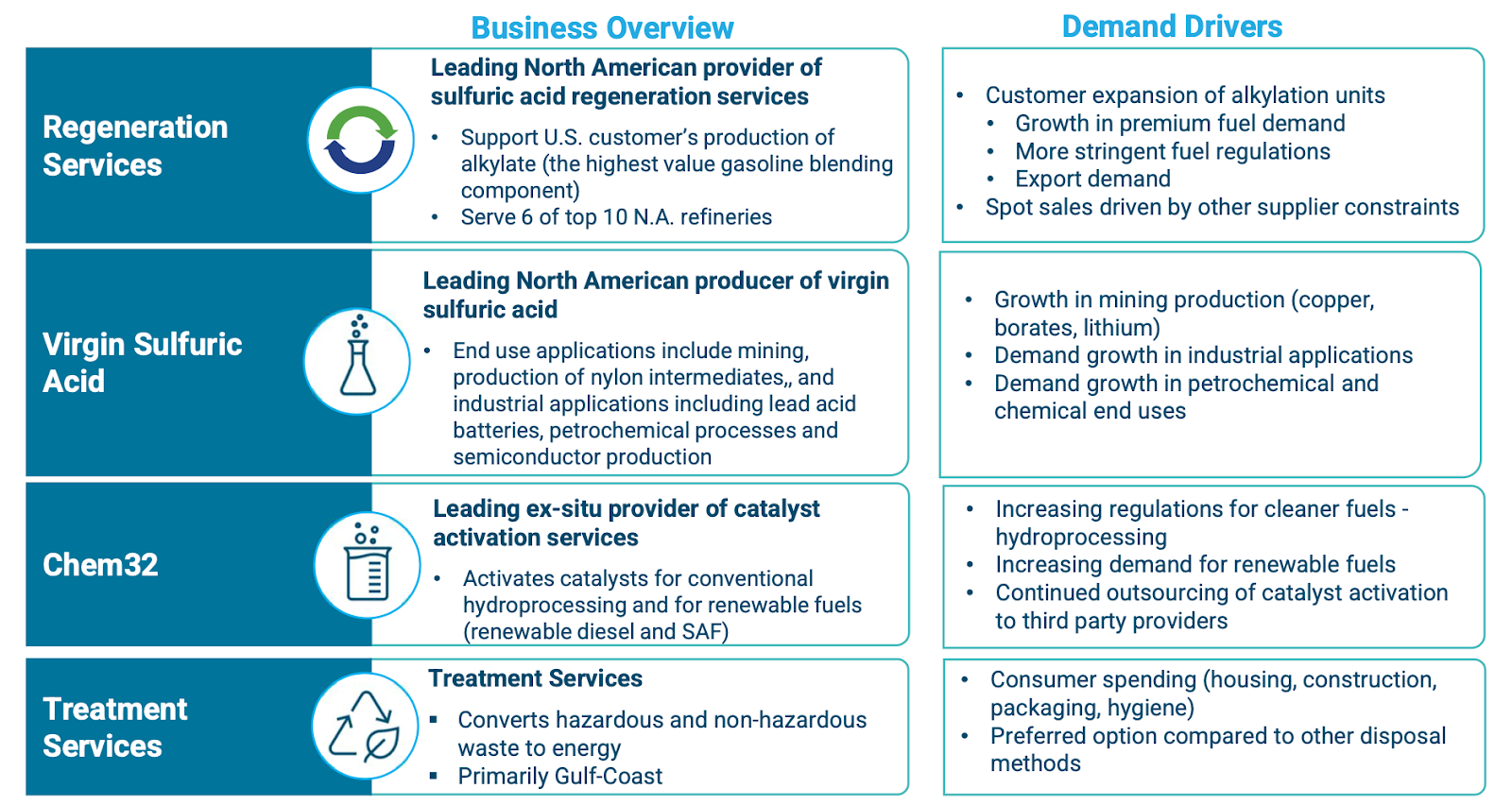

Ecovyst also produces virgin sulfuric acid, 20-25% of which goes to mining, another 20-25% to nylon precursors, and the remainder mainly to various industrial processes.

Management has commented on the very strong mining demand, citing rising copper demand from data centers, renewable energy, and EVs, plus tariffs/onshoring pushing more domestic production.

Overall, they expect long-term growth in sulfuric acid demand from U.S. mining and processing and have already turned on two expansion projects for existing mining customers in 2H25.

Nylon shows more near-term uncertainty due to overcapacity in Asia, but management expects demand to strengthen and likes the long-term outlook.

So, Ecoservices primarily recycles for refineries and produces for mining/industrial applications.

In their 2017-2022 reports, Ecovyst explicitly claimed to have the number one supply share in the U.S. in sulfuric acid regeneration with over 50% market share.

They stopped citing the 50% number after that, which makes me wonder (assume) if it has declined somewhat. Nevertheless, one of their top competitors with half the sales was sold in 2023, so it’s safe to say Ecovyst still holds a comfortable #1 market position.

So, so far we’ve established 1) sulfuric acid is a necessary product, 2) Ecovyst provides a necessary (cost and regulatory) service, and 3) they have the leading market share.

There’s a couple other things I like about this business.

First, their sales are contracted. Sulfuric acid recycling tends to be 5-10 year contracts; virgin sulfuric acid 1-5 years. Better still, ~90% contain some form of raw material pass-through clause.

These price adjustments generally reflect our Ecoservices segment’s actual cost structure in producing sulfuric acid, and tend to provide us with some protection against volatility in labor, fixed costs and raw material pricing. Freight expenses are generally passed through directly to customers.

We partner with many of our customers under long-term contract agreements, 100% requirement arrangements and/or specified products for certain licensed production processes. In our Ecoservices segment, approximately 50% of our production capacity serves customers with staggered multi-year commitment contracts with potential for value pricing resets and cost pass-through for our regeneration services product line that enhance sales and margin predictability and stability.

In 2024, they did more than 1.4M metric tons in regeneration volume. A large portion of the revenue per ton from this is just the pass-through of volatile costs like energy and freight. The profit comes from the tolling fee they charge for the regeneration service.

Because of that structure, plus minimum-volume protections and quarterly price adjustments for commodity inputs, labor, natural gas ,and the Chemical Engineering Plant Cost Index, they’re much more protected against raw material or energy price swings than a typical chemical producer.

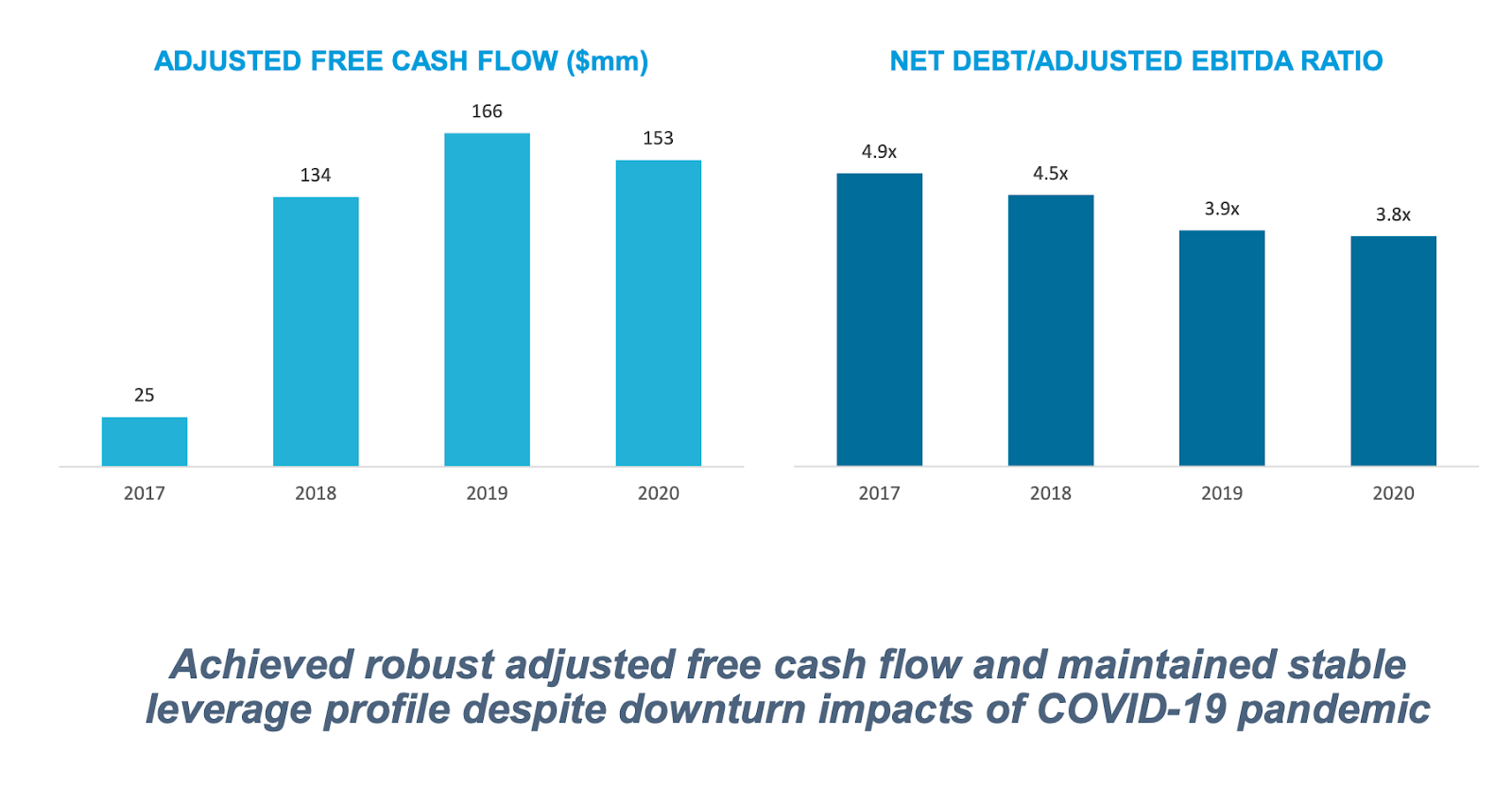

That provides a lot of protection and visibility, which is why they’re able to get 70%+ cash conversion and stable margins (dollars more so than percentages) through the cycle compared to something like PBF negative cash flow during COVID.

It’s not risk-free, though. Most major refineries can terminate the contract with 1-2 year notice. But, most of the relationships are long-term and it’s not a seamless transition for a refinery to replace Ecovyst.

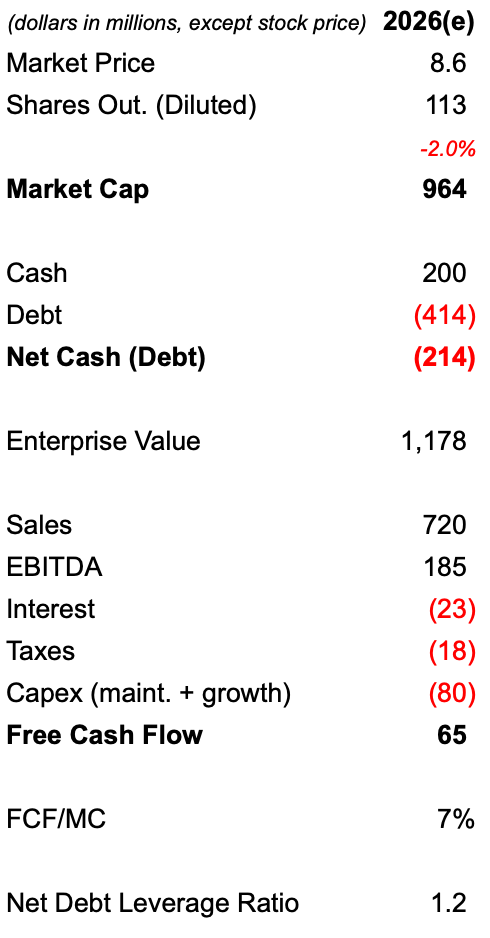

Speaking of divestitures (if you read the previous caption), Ecovyst is selling their Advanced materials & Catalysts segment to Technip Energies for $556M. The deal is expected to close 1Q26, and they plan to use $450-500M of the expected $530M net proceeds to reduce long-term debt, taking projected net debt leverage ratio below 1.5x.

Pro forma:

Post-close debt balance range: $364-414M

Post-close cash balance range: $150-200M

Expected net debt: $214M

On top of that, there are no significant maturities until 2031, no maintenance covenants on leverage, and interest rate caps to limit rate exposure.

I would pay $6.50-8.50 per share for this business. Ecovyst trades right at the high end of that range. So, why am I buying it?

I tend to be conservative. All else equal, if something trades in the range I come up with for myself, I’m fairly comfortable I won’t lose my shirt, and the upside is probably better than I expect. It's not foolproof. But it works for me more often than not.

One of the reasons Ecovyst is divesting is because they didn’t feel the market was properly valuing the combined segments.

Last July, Veolia sold its sulfuric acid regeneration business ($350 million revenues in 2023) to private equity firm American Industrial Partners for an enterprise value of $620 million. Ecovyst has twice the sales and ~50% market share.

The Board of Directors recently amended its existing $450M share repurchase plan to remove the April 2026 expiration date, $202.2M of which is still available.

That’s ~20% of Ecovyst’s current market cap. With minimal debt, my expectation is that they ramp up the repurchases – though, I also expect tuck-in acquisitions.

Net debt leverage ratio has historically been 3-3.5x. After the divestiture, the leverage ratio will be below 1.5x, which the CFO basically said is too low. Management is targeting 2-2.5x over time – depending on how aggressive they are with buybacks and M&A – and was clear that buybacks are the best way to create value aside from funding organic growth and tuck-in acquisitions.

I expect free cash flow in 2026 to be around $65M (including growth capex), and normalize higher than that. This year hasn’t been great for regeneration volumes with a refinery fire and some unplanned outages, but 2026 should look more normal.

But, using that $65M number and assuming zero growth, just with existing cash on hand + future earnings, they could (theoretically) retire ~10% of their shares outstanding 2026-2030, with no further deleveraging and end up with $60M cash and a net debt leverage ratio of 1.9x. That’d bring my fair value range to $9-14 per share.

The only bets I like to make are that I’m not going to lose a lot of money, and have a comfortable chance of getting a decent return without any real effort on the company’s part.

In terms of downside, I think the true value is unlikely to be more than ~20% below today’s price unless you get something extreme, like refinery closures or a shift away from sulfuric acid alkylation.

More likely, I own a business that is throwing off a fair amount of cash and can retire a meaningful amount of stock over time at a fair price, producing low double-digit annual returns.

If management delivers mid-single digit growth in volume and contract pricing, that on top of buybacks and any multiple or margin expansion – and then there’s always a chance someone acquires them, which I’d expect would happen at something like 50%+ above today’s price.

Risks

One concern is that I've seen a lot of commodity-esque businesses with “contracted cash flows” who use it all to buy out the PE sponsors who took them public. It often doesn’t end well for the remaining shareholders. To an extent, that’s already played out.

Ecovyst was taken public in 2017 by private equity firm CCMP Capital and INEOS Group, the ninth largest chemical company in the world by sales.

After that, Ecovyst sold a couple segments in 2020 & 2021, paid out two special dividends, and used a $450M share repurchase program to help CCMP exit.

I don’t view repurchases at current prices as a bad thing, and am not worried about the long term trends of the business. I just recognize this pattern and have seen it go wrong many times.

Repurchases are one side of what Ecovyst wants to do, and the other is the second risk: acquisitions.

Post-divestiture, Ecovyst will have a strong balance sheet and cash flow profile. I expect they’ll at least do some tuck-in acquisitions, similar to the Waggaman sulfuric acid regeneration plant/assets they acquired from Cornerstone Chemical for $41M ($35M purchase price + $6M adjustments for working capital) in May 2025 (Cornerstone Chemical spent $36M building the plant).

So far, Ecovyst has benefited from Waggaman’s network with more tankage in Houston, more capacity and efficiency at Waggaman, and debottlenecking projects behind that. Management said a lot of the inherited Waggaman contracts roll off and get repriced into 2026, so we should see more tons and better pricing.

That’s the kind of deal I’m okay with. As long as they don’t overpay and overleverage, I think this works out decently.

Summary

Ecovyst is a durable business inside a more volatile industry. I think it’s reasonable at today's price and has a good chance of producing low double-digit returns over the next few years, with more upside if the market comes to appreciate the simplified structure and dominant market share, or if they are acquired.

I know, who cares about a ~10% IRR when there’s multibaggers to be had (so they tell me). I’m not particularly keen to have a lot of commodity exposure right now. It feels like a good time to exercise some caution which is why half my portfolio is liquidations and take-privates. ECVT is attractive to me in that context. It's more conservative, has a clear path for capital returns and/or a possible take-out, but still benefits from things like a bull market in mining.

Disclosure

I spent more time reading about Venus's atmosphere than I did Ecovyst. Do your own work.

Member discussion