Buffett Has Lost It -- Kraft Heinz

I don’t think Charlie and I…certainly at Berkshire…I don’t think we’ve ever had a permanent loss in marketable securities that was — what? — 1% maybe? Half a percent of net worth? — Warren Buffett, 2007 AGM

Kraft Heinz is frequently cited as one of Warren Buffett’s worst investments.

Just look at the Kraft Heinz stock chart.

That doesn’t look promising. Plus, he even admitted Kraft was a mistake.

But, since no one seems to be doing more than posting stock charts – if that – I thought I’d put numbers next to the take.

Before we get started, this is not investment advice. This is not an argument or research for Kraft Heinz stock (KHC) – even though I own some.

This is simply about the stupidity of tweets and headlines I see which talk about how much money Buffett has lost on KHC.

Here’s the tl;dr: Buffett has actually gotten more than a 6% CAGR on his Kraft Heinz investment [$7B+ in profit] from June 2013 to September 2025.

Everything after this is just supporting evidence and historical context.

Background

Buffett’s Kraft Heinz investment predates the Kraft Heinz merger.

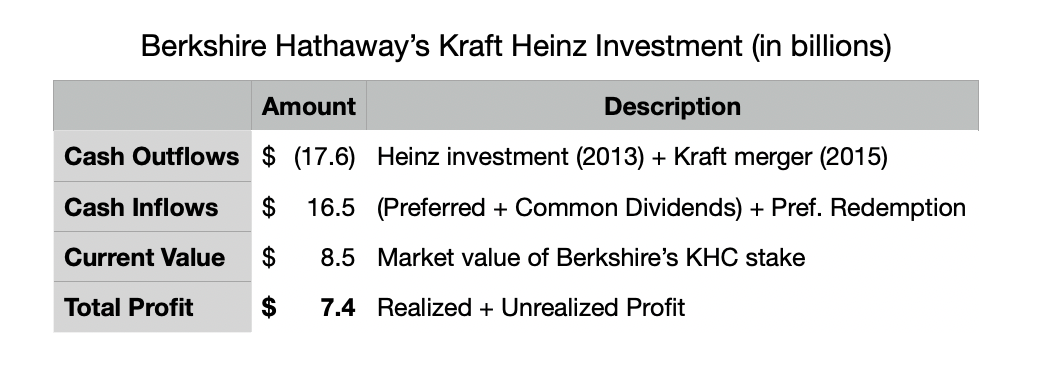

In June 2013, Berkshire partnered with 3G to take Heinz private. Berkshire invested $12.25B total in $8B par value 9% cumulative preferreds plus common stock and penny warrants.

Then, in July 2015, Heinz merged with Kraft. Berkshire added $5.4B additional capital to buy newly issued Heinz/Kraft stock.

Cost basis

I read one write up – one of the only ones who tried to support their opinion with actual numbers – where the author took the “Investments in The Kraft Heinz Company and other investments” line of the 2015 Berkshire Hathaway cash flow statement, and attributed every cash outflow on that line for 2013-2015 to the cost basis of Buffett’s Kraft Heinz investment, causing an overstatement of $3B (2014) on the cost basis.

If you look at the 2016 Berkshire Hathaway cash flow statement, you see they separated the Kraft Heinz and “other investments” and the $3B is no longer on the Kraft Heinz investment line. You can also double check this against Buffett’s 2016 commentary.

In his 2016 letter, Buffett said point blank: Berkshire’s cost for the Kraft Heinz common stock was $9.8B. Easy enough to check: $12.25B (preferred + common) + $5.4B (additional Kraft/Heinz investment) - $8B (preferred) = $9.65B common stock cost basis. Close enough.

People citing equity-method values or posting a KHC stock chart have already lost the plot. The former adds non-cash adjustments every year and the latter doesn’t incorporate the fact that the majority of Buffett’s investment was put on with H. J. Heinz before it merged with Kraft.

XIRR

If you don’t know what XIRR is, it’s an IRR calculation for lumpy cash flows. Because Berkshire has invested and received various amounts of cash at different times, you use XIRR to find the return.

So, if you run the XIRR on all the cash inflows and outflows of their investments plus preferred and common stock dividends from June 2013 to September 2025, you’ll get ~6.2%.

That is to say, Buffett has not lost money on his Kraft Heinz investment. Not the preferred stock and not the common stock.

It may have been a mistake. A 6.2% CAGR may not be the greatest return ever. He may be looking to sell. But there is no permanent loss of capital to be found.

Frequent Comments

“Buffett lost money.” No, he hasn’t.

“The opportunity cost was huge. He should’ve indexed.” Anything that lags the index looks worse than the index — tautology noted.

The broader point stands: Buffett’s worst mistakes rarely cause a permanent loss of capital. In the few cases where it does, it’s very minimal relative to Berkshire’s net worth.

Again, this is supposed to be one of Buffett’s worst investments. Ever.

Make a list of your worst investments. Did one of the ones that made the list CAGR at 6%? And let’s revisit this question after you’ve been investing for three quarters of a century.

Also, for context, when Buffett bought Heinz with 3G in 2013, the investment was proportional to ~5.5% of Berkshire’s equity. The majority of that being preferred shares. After the Kraft merger, the total investment was less than 7% of Berkshire’s YE2015 equity. Today, the remaining Kraft Heinz stake is worth ~$8.5B versus $670B of equity on Berkshire’s balance sheet.

Here’s the bottom line. Buffett didn’t lose money on Kraft Heinz. Berkshire Hathaway stock returns have been in line with the S&P 500, or outperformed, on basically every meaningful time period. That’s with a large cash drag and substantially less risk.

“The only reason Berkshire has done well is because of Apple stock. If you take that out, Berkshire’s returns are worse.” My favorite response here is from @zugmanfabio who tweeted, “If my uncle didn’t have a dick he would be my aunt.”

Buffett did invest in Apple.

“But it wasn’t his idea.”

Okay person who reads 13-F’s, newsletters and/or Twitter threads. I’m sure you have originated every investment idea you’ve ever had on your own.

Yes, Buffett’s lieutenant first invested. Buffett thought about, and ultimately put on ~95% of the position.

If you want to live in hypotheticalville, go for it. You don’t have to like Warren Buffett. You don’t have to own Berkshire Hathaway. You aren’t required to be a value investor.

But, before you go around judging someone with a much better track record in every way than you’ll ever achieve, maybe run the actual numbers and look at reality, not “what ifs” and “if you strip this out then hypothetically…”

And before someone says, “you’re cherry picking his mistake. X, Y & Z are worse.” I’m going to cover those too.

The man is a god damn legend.

Member discussion