ARC Document Solutions (ARC)

This was an idea I posted on Twitter last summer. It is a review of ARC Document Solutions (ARC) after management and a private investor submitted a non-binding proposal to take the company private.

It was a high probability bet of a quick transaction with limited downside and potential for a price increase.

The Catalyst

On July 2, 2024 the Board of Directors of ARC Document Solutions announced it had received a non-binding proposal from an acquisition group led by ARC’s CEO, Kumarakulasingam Suriyakumar.

The acquisition group already owned ~19.6% of the shares outstanding. The offer was to acquire the remaining outstanding shares of the company for $3.25 per share in cash.

The Company

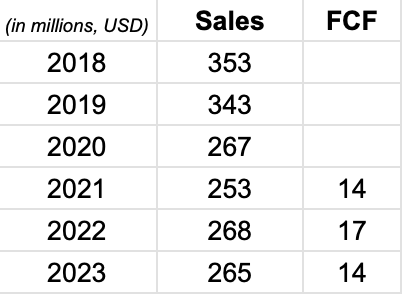

ARC offered digital printing solutions for businesses. The business had been in a long state of decline, but the last few years had seen sales relatively stabilize:

ARC had spent the last several years deleveraging (they paid down $110M in six years), to the point where they were net debt free. The balance sheet was:

- Cash/Equivalents: $52M

- Receivables: $38M

- Payables: $24M

- Debt/Finance Leases: $61M

The $3.25 per share cash offer price put the market cap around $140M.

The Thesis

The proposal was likely to be accepted and consummated in short order for several reasons:

- The CEO’s proposal to the Board cited several logical reasons for taking the company private:

- Declining long-term operating performance

- Negligible investor interest in the stock

- Ongoing costs of being public

- Managing the dividend and buyback policies and investor sentiment given business uncertainty

- The acquisition group already controlled nearly 20% of the company.

- Management had received egregious compensation every year since the IPO, demonstrating a “friendly” BoD.

- U.S. Bank, who provided ARC’s existing revolving credit, was willing to finance the deal.

- Each quarter the deal took to close would add an additional $0.05 per share on top of the $3.25 offer price from dividends.

The Valuation

Some investors felt the offer was too low. They calculated free cash flow as operating cash flow of $36.5M minus capex of $10.7M and thought management was buying the business for ~5x FCF.

However, (1) operating cash flow pre-working-capital adjustments had been declining every year ($48M in 2018 to $32M in FY23), and (2) you had to deduct finance leases.

As interest rates rise, capex increases as they buy equipment outright versus leasing, but current finance leasing is still a capex cost.

That led to an additional ~$12M in finance lease costs to subtract from OCF, bringing free cash flow to ~$14M.

The stock traded ~15% lower before the announcement. With the offering price seeming fair, the downside seemed capped if the deal failed unexpectedly.

You’d have a net-debt-free, profitable company paying you a 6%+ yield on cost. Not the worst thing ever.

The Agreement

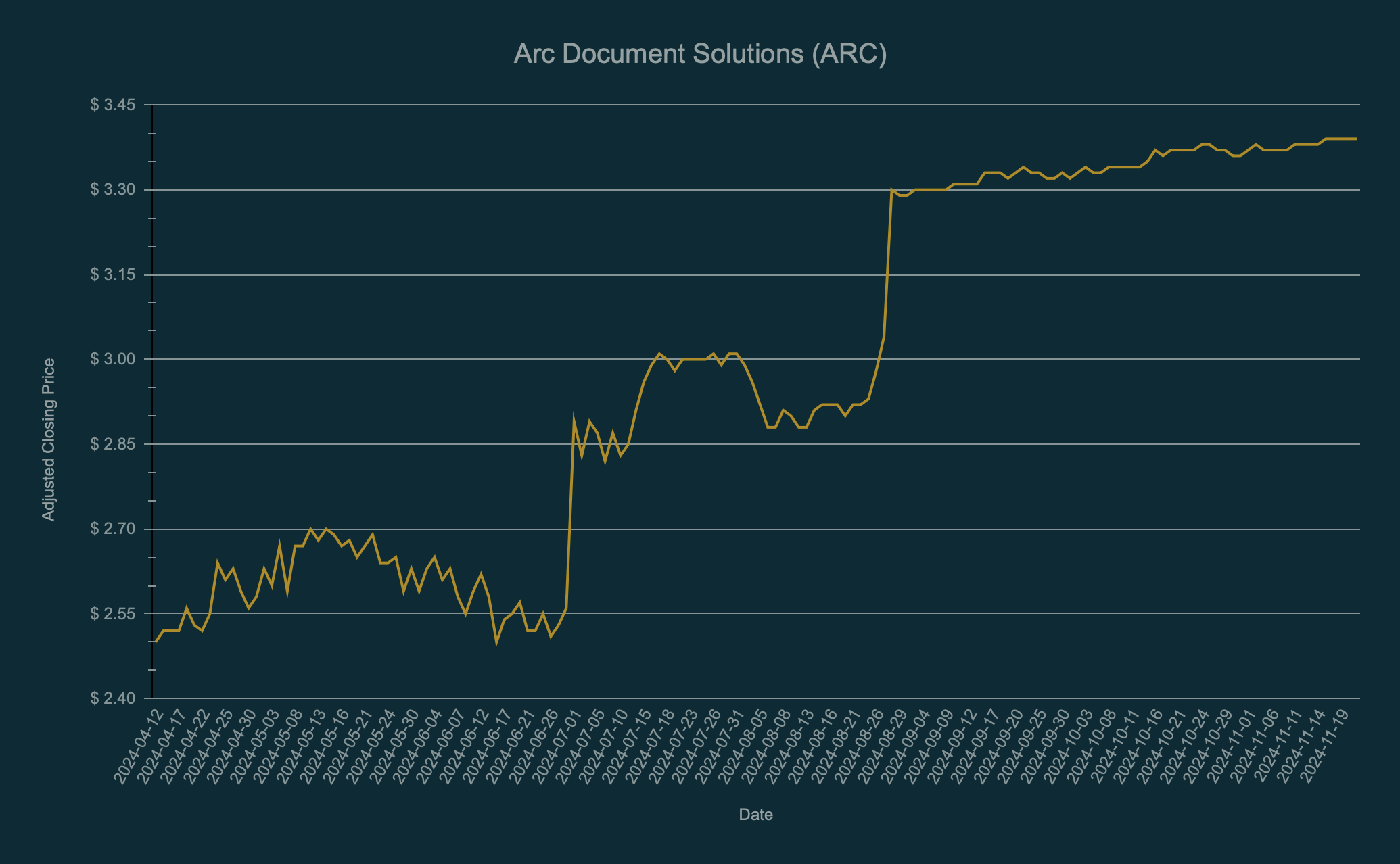

I got in at ~$3 per share cost. By the time I posted the idea on Twitter, the stock was around $3.08.

While the stock was small and illiquid, I figured given how many people like doing odd-lot trades for a $100 return, you could scale an idea like ARC more.

As I said, I was late to catch the announcement. But if you followed along, you actually got several weeks to accumulate shares below $3.

At the end of August, a definitive merger agreement was signed, with the take-private price being raised from $3.25 to $3.40.

The merger was expected to close by the end of the year.

The Outcome

I sold my shares the day the definitive merger was signed.

I received one $0.05 dividend + $3.31 sale price on a $3.01 cost basis.

An entry price of $3.08 – the price on the day I tweeted about the idea – along with a dividend and selling at $3.31 earned an XIRR of 111%, or 9% absolute return in 44 days. The SPY did -1% absolute return during the same period.

You could have also held until the deal closed, where the XIRR would fall to 44% but you got a 14% absolute return in 130 days.

The End

This is one of my favorite types of bets, where it required little brainpower to figure out:

- How much cash is there?

- When will I get it?

- How sure am I?

Member discussion